Investing can feel overwhelming, especially when your schedule is packed, your notifications are buzzing, and your to-do list never seems to end.

But what if you could grow your wealth without constantly checking the stock market, calculating returns, or stressing over every market dip? That’s where the “set it and forget it” investment plan comes in.

This guide will show you how to automate your investments, minimize stress, and still make your money work for you, without requiring hours of attention every week.

Why Busy People Need a “Set It and Forget It” Plan

For many, the biggest barrier to investing isn’t money, it’s time. Busy professionals, parents, and entrepreneurs often postpone investing because it feels like another chore. But here’s the truth: you don’t need to be glued to the market to build wealth.

A “set it and forget it” plan allows you to:

- Automate contributions: Your investments grow while you focus on life.

- Avoid emotional decisions: You won’t panic-sell during market dips.

- Leverage compounding: Even small, regular contributions add up over time.

Think of it as planting a tree, you water it consistently, but you don’t dig it up every day to see if it’s growing.

Step 1: Define Your Financial Goals

Before investing a single dollar, it’s essential to get crystal clear on why you’re investing. Your goals dictate your strategy, risk tolerance, and investment timeline, and they help you stay focused when the market fluctuates.

Short-term goals (1–5 years):

- Emergency fund: Build a safety net to cover unexpected expenses without touching investments.

- Vacation or home improvements: Plan for planned expenses so you can enjoy life without financial stress.

- Buying a car or other large purchase: Ensures you have funds ready without relying on high-interest loans.

Long-term goals (5+ years):

- Retirement: Build a nest egg to maintain your lifestyle and financial independence later in life.

- Buying a home: Plan for a down payment or mortgage payoff.

- Financial freedom: Create passive income streams and investments that eventually cover your living expenses.

Keep goals specific, measurable, and time-bound. Instead of “I want to save money,” say, “I want $50,000 for a down payment in 5 years.” Clear goals help you design a realistic investment plan and measure progress along the way.

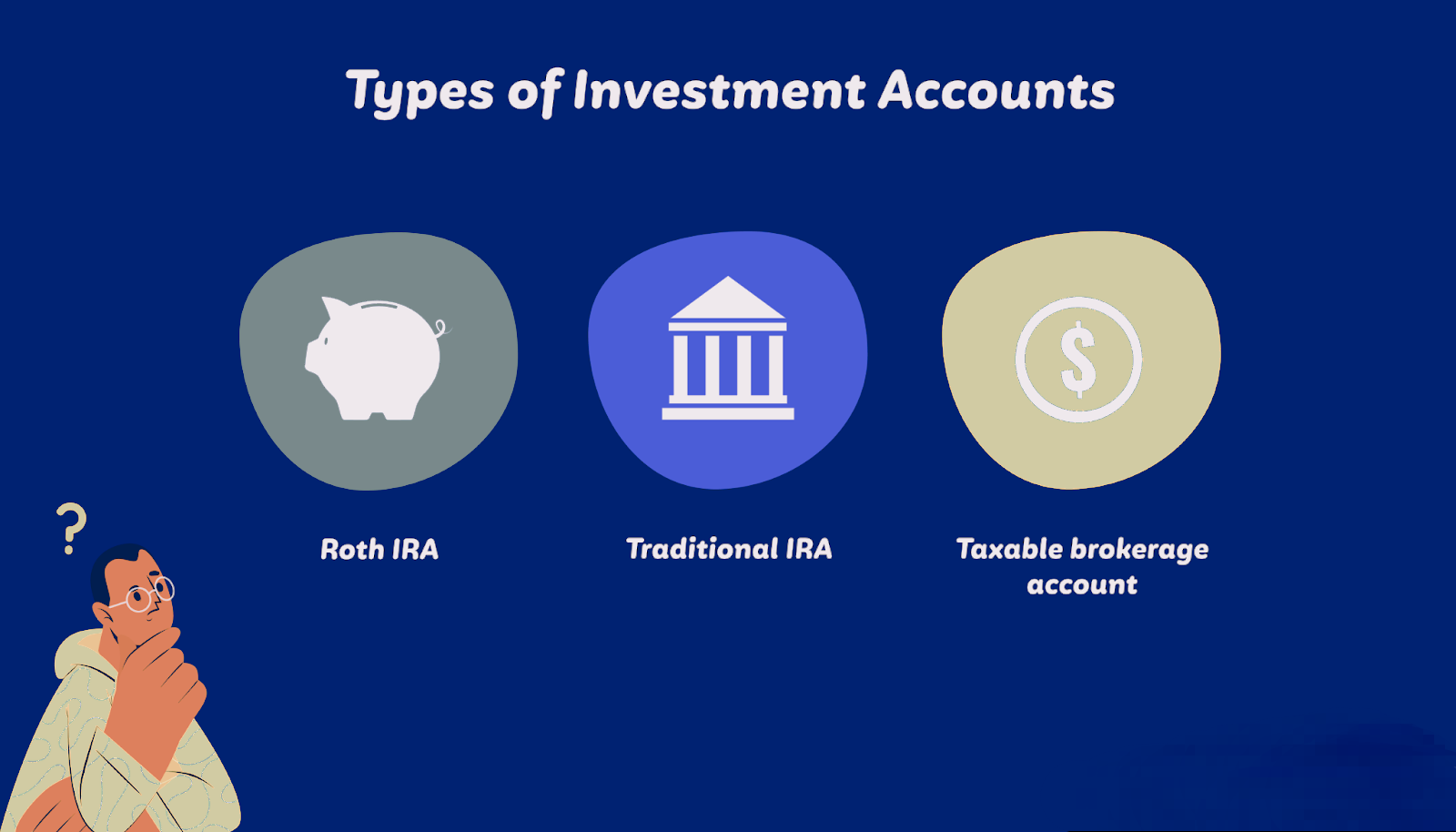

Step 2: Choose the Right Investment Accounts

Where you put your money matters. Different accounts affect taxes, accessibility, and growth potential, so picking the right one is key to maximizing returns.

- Brokerage accounts: Flexible accounts for investing in stocks, ETFs, and mutual funds. Ideal for non-retirement goals or funds you may need in a few years. Earnings may be taxable, but there’s no withdrawal restriction.

- Retirement accounts (401k, IRA): Tax-advantaged accounts for long-term growth. Contributions may be tax-deductible, and earnings grow tax-deferred. Roth options allow tax-free growth and withdrawals in retirement. These accounts are best for long-term goals like retirement or financial independence.

- Robo-advisors: Automated investment platforms like Betterment, Wealthfront, or M1 Finance select a diversified portfolio, rebalance it periodically, and manage risk for you. Ideal for hands-off investors who want professional guidance without actively managing trades.

If your employer offers a 401k match, prioritize it. It’s essentially free money and an instant return on your contributions.

Combine this with a clear understanding of your goals and suitable accounts, and you’ll have a strong foundation for consistent, stress-free investing.

Step 3: Decide on Your Investment Strategy

Once your financial goals and accounts are in place, it’s time to choose a strategy that aligns with your risk tolerance, timeline, and comfort level. The right strategy ensures your money works efficiently toward your goals without causing unnecessary stress.

Passive Index Funds

These are low-cost funds designed to track a specific market index, like the S&P 500. They offer broad market exposure and historically strong long-term growth. Ideal for beginners or anyone who wants a hands-off approach.

ETFs and Diversified Portfolios

Exchange-Traded Funds (ETFs) allow you to spread your investment across multiple industries or asset types, reducing risk.

For example, a mix of tech, healthcare, and consumer ETFs can balance growth potential and stability. Diversification is key to minimizing losses during market dips.

Dividend-paying Stocks

These stocks provide regular income through dividends while also giving potential capital appreciation. Dividend reinvestment plans (DRIPs) allow you to automatically reinvest dividends, compounding your returns over time.

Key principle: Simplicity beats complexity. You don’t need to pick individual stocks or time the market. Broad market funds or ETFs can generate substantial long-term returns with minimal effort, making them perfect for a “set it and forget it” plan.

Step 4: Automate Contributions and Investments

Automation is the core of a “set it and forget it” strategy. By automating, you eliminate friction, reduce missed contributions, and make investing a natural habit rather than a chore.

Set up Recurring Transfers

Schedule automatic transfers from your checking account to your investment accounts, weekly, biweekly, or monthly. Treat this like any essential bill, ensuring consistent contributions.

Automate Allocations

Many platforms allow you to pre-set your portfolio allocation (stocks vs. bonds vs. ETFs). Your money is automatically distributed according to your chosen plan, keeping your investments balanced over time.

Use Apps and Tools for Automation

Platforms like M1 Finance, Vanguard, Fidelity, or Robinhood make recurring investments simple. Some even automatically rebalance your portfolio as market conditions change, maintaining your target allocation without manual intervention.

Think of investing like paying rent or utilities. Once it’s automated, you remove decision fatigue and human error, allowing your money to grow steadily while you focus on life. Even small, consistent contributions compound over years into meaningful wealth.

ALSO READ: Is This Investment a Scam? 5 Red Flags to Spot Immediately

Step 5: Minimize Fees and Taxes

Even small fees and taxes can quietly erode your investment gains over time. Being mindful of these costs is one of the easiest ways to boost long-term returns without taking on more risk.

Choose Low-Cost Funds

Index funds and ETFs with expense ratios below 0.5% are ideal. Over decades, high fees can compound into thousands of dollars lost, so keeping costs low is crucial.

Use Tax-Efficient Accounts

Tax-advantaged accounts like IRAs and 401(k)s allow you to defer taxes or even avoid them on certain gains. Roth IRAs, for example, let your investments grow tax-free, which is a huge advantage over the long term.

Avoid Frequent Trading

Every time you buy or sell, you may trigger fees or capital gains taxes. Frequent trading also increases the risk of making emotion-driven mistakes. A buy-and-hold strategy often outperforms active trading for most investors.

Think of Fees Like Termites

They’re small and often invisible, but left unchecked, they can quietly destroy your wealth over time. Minimizing costs ensures your money compounds as efficiently as possible.

Step 6: Avoid the Common Pitfalls

![]()

Even with automated investments, mistakes can slow growth or reduce returns. Awareness is key to staying on track.

Overreacting to Market Swings

Markets fluctuate naturally. Panic selling during dips locks in losses and prevents recovery. Remember, volatility is normal, and downturns are often temporary.

Frequent Portfolio Tinkering

Constantly adjusting allocations or chasing “hot stocks” adds stress and can reduce long-term gains. Stick to your plan and let compounding work its magic.

Ignoring Inflation

Inflation erodes the purchasing power of money. Investments must grow faster than inflation to preserve and increase real wealth. Low-interest savings accounts alone often don’t keep pace.

Keep emotions out of investing. Automation combined with patience is more powerful than any short-term strategy. Trust the process, revisit your plan periodically, but resist the urge to micromanage.

Step 7: Monitor Progress Without Overthinking

You don’t need to obsess over daily market movements. Checking in too often can lead to stress and impulse decisions. A simple, quarterly review is sufficient for most investors.

Quarterly Check-Ins

Every three months, review your account balances, contributions, and portfolio allocation. Ensure your investments are still aligned with your financial goals.

Use Dashboards for Clarity

Tools like Personal Capital, Mint, or Vanguard’s portfolio view provide a clear snapshot of your holdings, performance, and diversification, so you can see the big picture at a glance.

Adjust Only if Necessary

Life changes, such as a new job, a major purchase, or a growing family, may require tweaking your contributions or risk allocation. Avoid reacting to short-term market swings; only make changes if your long-term plan demands it.

The goal is stress-free growth, not constant worry. Treat your investments like a slowly growing tree: water it consistently, check occasionally, and let time do the rest.

Step 8: Advanced Tips for Busy Investors

Once your system is up and running, these strategies can optimize growth with minimal effort:

Automatic Rebalancing

Some platforms automatically rebalance your portfolio to maintain your target risk level. This ensures you don’t become unintentionally overweight in one asset class after market fluctuations.

Dollar-Cost Averaging (DCA)

Invest a fixed amount regularly, regardless of market conditions. This strategy reduces the impact of volatility, buying more shares when prices are low and fewer when prices are high. Over time, this smooths out market fluctuations.

Plan for Long-Term Growth

Account for inflation, future contributions, and major milestones like retirement, buying a home, or funding education. Setting these targets early ensures your portfolio grows in line with your life goals.

Use Automation Wisely

Combine recurring contributions, robo-advisors, and auto-rebalancing to maximize returns without adding complexity. Your money continues to work for you, even when life gets busy.

With these advanced strategies, you can optimize growth while maintaining a truly “set it and forget it” approach, building wealth passively, reliably, and with minimal stress.

Conclusion: Building Wealth While Living Your Life

The beauty of the “set it and forget it” plan is that it works in the background. You can focus on your career, family, hobbies, or travel, while your investments quietly grow.

Consistency, patience, and smart automation are the keys. Even if you start small, regular contributions and long-term thinking can turn your busy life into a wealth-building machine.

You don’t need to be an investing expert or check the market daily. With a plan, automation, and minimal oversight, your money can work for you, while you focus on living your life.